The thought of losing money can be a primary driver when it comes to investment decision making. When people think of risk, in terms of investing, it almost always means seeing the value of their money going down.

It boils down to a fear that it could be worth less now than when you started or ‘you may not get back part of your initial investment’, meaning we can’t do what we want with it in the future. After all cash in the bank does not go down in value, right?

These emotions can be even more heightened when you have the responsibility of looking after someone else’s money, in the form of a charity or trust.

But what does that safety of cash in the bank cost us in reality and can we challenge our perception of what risk actually means?

Keeping money in the bank may seem like the safe choice, after all it won’t go down. £100 will still be £100 in 5 years’ time (and if you are lucky you may get a bit of interest on top of that in exchange for giving up access to it for a fixed period). However, what happens if the plans you had your eye on have become more expensive, what if it is now going to cost you £150? You can no longer afford it, or you have to spend more cash than you planned.

The rate of inflation – the rate of increase in prices, has eroded the value of your cash in the bank. The years since 2022 (to the end of April 2026) are a recent example of the power of inflation. It may have seemed that 4-5% interest from the bank was a good return and compared to the last 10 years even reasonably attractive, but in reality, if prices are rising then your money will have still been losing value. In ‘nominal terms’ (the number of pounds in your account) your cash was increasing in value as it grew by 4% each year, but in ‘real terms’ (what those pounds will actually buy you) its value was falling, due to the impact of inflation.

Over that period, since the start of 2022, UK prices (measured by CPI) increased by 23.5%. Compare that to the return of 18% you would have got on cash held in the bank and remember interest rates were at the highest levels for 15 years over that time. Then compare that to the 56.5% return of a global equity index such as the MSCI world. Money invested in the shares of global companies would have generated 3 times the return of cash.

What this means is, in 2026 the money held as cash in the bank will not buy you as much as it did at the start of 2022, but money that had been invested over that time will now buy you more.

This is the impact of inflation and makes it the number one risk to our future financial goals, highlighting the not always immediately obvious risk - inflation is the real enemy. There is therefore a risk that being over cautious with the assets that we have, although feeling like a safe and prudent decision, can negatively impact our longer-term goals or the impact that this money can have in the future. Indeed, there is a longer-term cost to being over cautious; being too cautious is itself a risk!

We have to ask ourselves; do we have longer term goals that are likely to be impacted by inflation (very few are not) and do we need to do something now to mitigate against it?

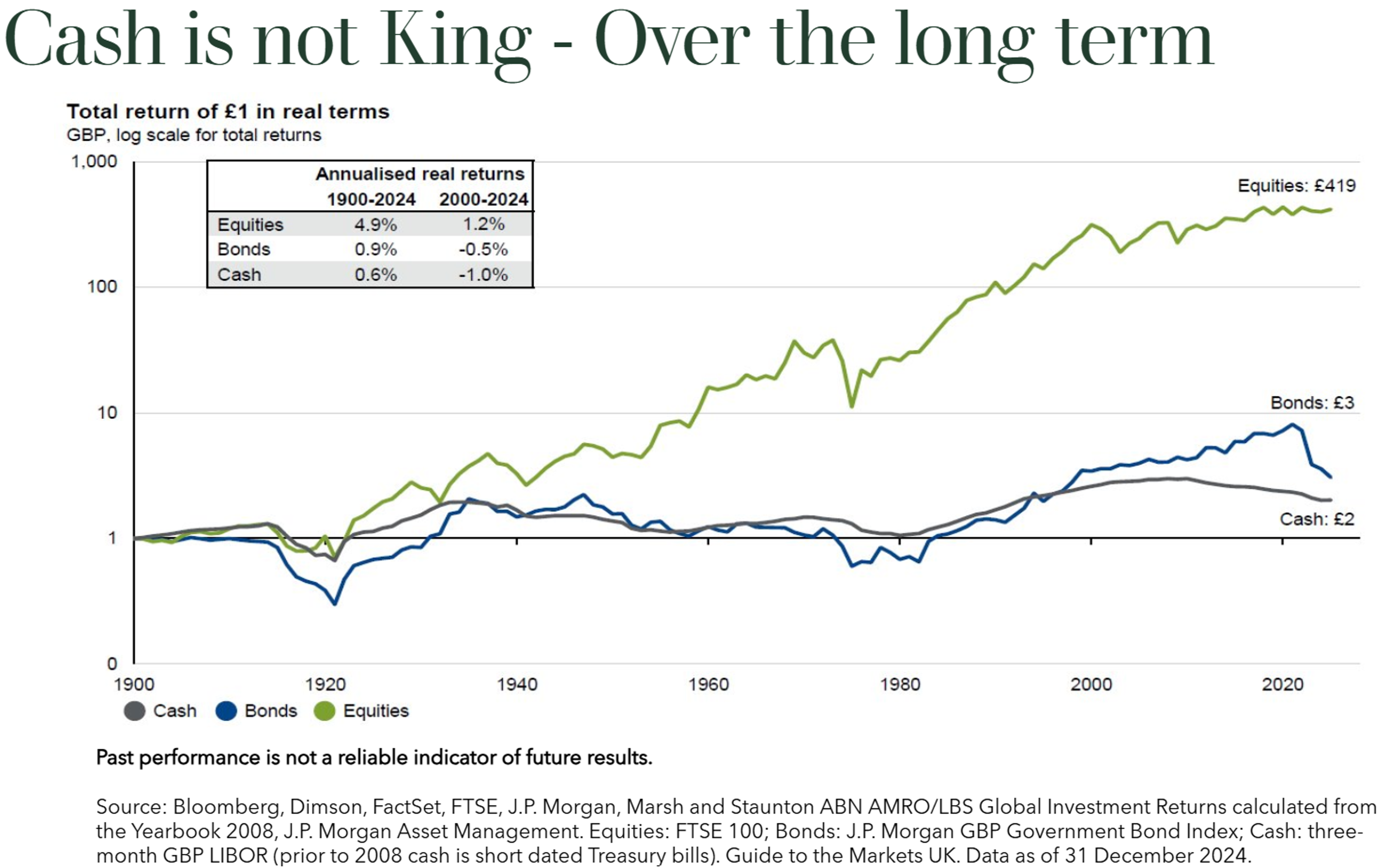

The below chart shows what would have happened in real terms (taking inflation into account) to £1 invested over the last 120 years. It shows that only equities have managed to deliver the sort of returns that will beat inflation.