Summary:

- UK outperformance driven by structure: The UK market has recently benefited from its tilt toward asset-heavy sectors like Energy and Materials, which have gained amid AI‑driven rotation, higher real interest rates and demand for infrastructure assets.

- Global diversification still key: Despite strong UK performance, global markets offer far broader opportunities, with regions such as Japan providing appealing structural growth potential.

- Disciplined global approach: The recent UK gains don’t alter the case for maintaining a globally diversified portfolio—focused on fundamentals, balanced exposure and long‑term resilience.

Understanding the structural shifts behind recent market moves

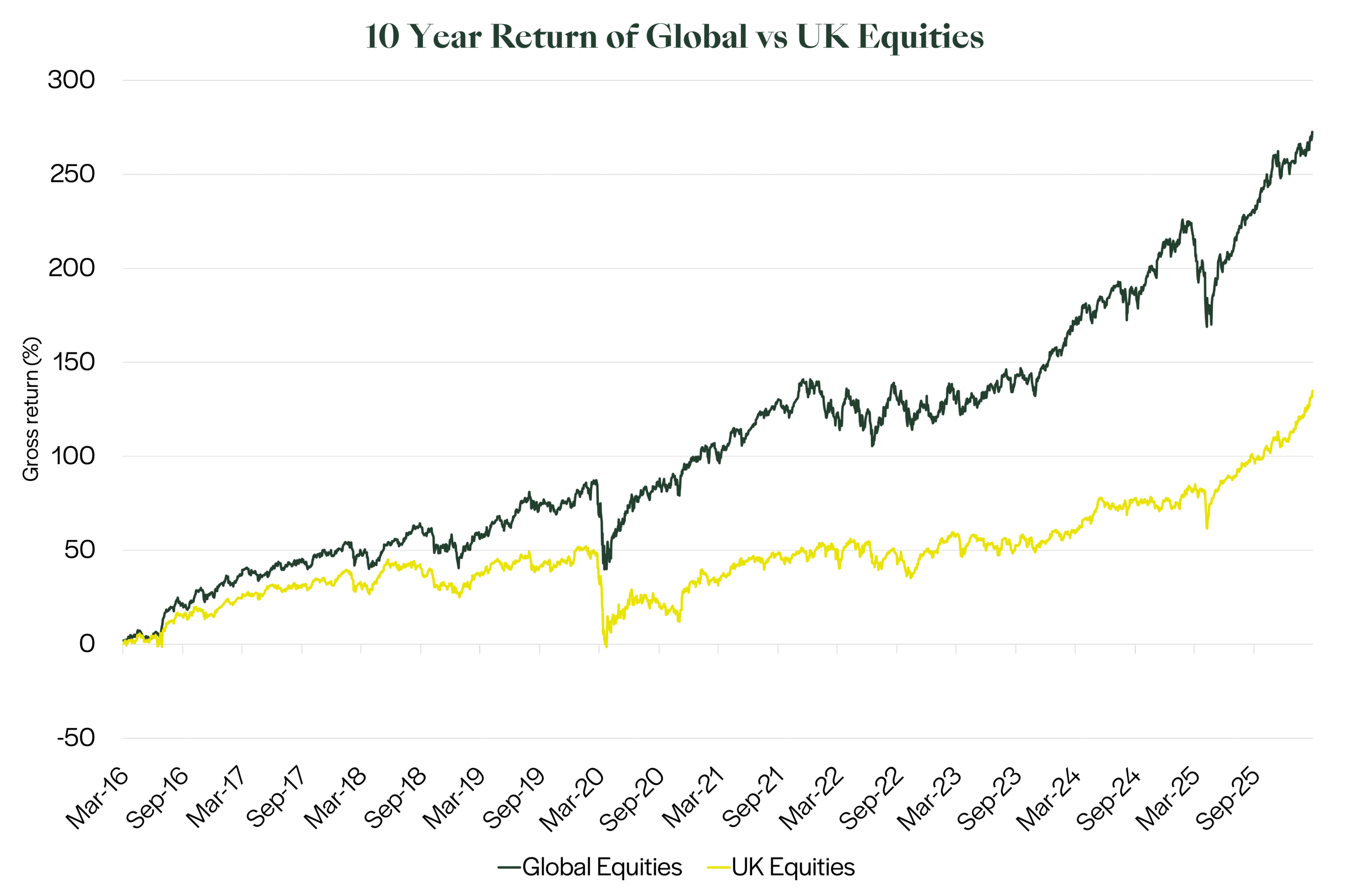

With US equites lagging and emerging markets outperforming in 2026, regional equity performance (that is, the performance of equity investments across different geographic regions) has re‑entered the spotlight this year. The UK stock market has delivered a notably strong performance, relative to the US and global equites more broadly. These regional shifts in performance can feel abrupt, but much like geopolitical developments, the forces driving them tend to unfold over longer cycles. Short‑term moves matter, but the real insight comes from stepping back and understanding the deeper structural changes shaping the performance of markets over time.

In this article, we explore what’s been driving the recent UK market performance, how technological disruption is influencing regional market leadership, and why global diversification remains at the heart of our approach: even during periods of outperformance for specific regions, we believe a more global stance pays off over the long term.

The forces behind recent regional divergence

- Artificial Intelligence (“AI”) has been reshaping market leadership

Recently, investors have been discerning of AI related opportunities and risks, and have leant toward “old‑economy” areas such as Energy, Materials, Industrials and Utilities. These sectors rely on physical assets and real‑world infrastructure, which have been perceived as both harder for AI to disrupt, and partial beneficiaries from AI investment expenditure in the near term. This shift has naturally supported the UK market because it has more companies in these industry groups. - Markets have been rewarding businesses built on “tangible” assets

Higher real interest rates (interest rates with the rate of inflation removed), supply‑chain pressures and a focus on security of supply have increased demand for companies that own essential infrastructure. Examples include power networks, pipelines, refineries and resource producers. This trend has also benefited the UK market recently, which has a higher exposure on average to sectors like Materials, Utilities, and Energy compared to global benchmarks. - Value has taken the lead

After years of technology-led dominance from high growth companies, so called “value” companies (companies that appear cheaper with higher earnings relative to price) have been outperforming since late last year. This has also helped the UK’s recent relative performance, although history shows these leadership shifts are rarely permanent.

We are taking a measured stance on UK equities

Against this backdrop, a question we hear currently is: why do we prefer Global equities to UK equities?

While we are broadly neutral in our outlook on the UK market relative to global equity benchmarks at the current time, our portfolios generally have a lower allocation than many of our peers (or peer benchmarks).

Despite the UK’s recent resilience, our fundamental view has not changed: a globally diversified portfolio provides a better long-term opportunity set for returns, while bringing additional diversification to help manage volatility along the way.

We see the UK as one important part of a much wider global opportunity set:

- The UK represents less than 4%of the global stock market[1], and while it is home to many high-quality businesses, the breadth of opportunities available across global markets is significantly larger.We believe investors should consider their allocation to equities through a wider global lens, rather than focusing too heavily on any single market.

- While many UK-listed companies are world-class firms with international revenue streams and strong competitive positions, other regions currently offer particularly compelling structural opportunities. Japan is one example, where we see a supportive domestic macroeconomic backdrop and encouraging corporate governance reforms.

This is not a comment on the quality of UK companies. Many are world‑class exporters with diverse revenue bases. Rather, it reflects the depth and breadth of the global opportunity set relative to any single market. We believe the most sensible approach is to look globally and maintain broad diversification across regions, including an allocation to the UK.

The domestic UK economic backdrop is stable, but not transformational

At the start of the year, the outlook for the UK was beginning to improve. Inflation was expected to continue falling, which would have given the Bank of England scope to lower interest rates and offer some support to economic growth and the labour market. This would have been a constructive backdrop for the more domestically focused parts of the market, although it still wouldn’t have changed the UK’s longer‑term return profile relative to global equities. Global markets were also well positioned to benefit from solid growth expectations as the year began.

The recent US–Iran conflict has introduced a new source of uncertainty. A more prolonged or wider escalation could keep energy prices higher for longer and delay expectations of rate cuts, which in turn affects the outlook for consumers and businesses.

The structure of the UK economy adds further nuance. The UK has a relatively small manufacturing base and a large service sector, where many roles are being reshaped by technology and AI. This leaves the economy more sensitive to changes in global demand, evolving technology trends and shifts in competitive pressures. While this creates selective opportunities, it does not yet make the UK a stronger long‑term equity story than the broader global market, in our view.

Why we remain more global than peers

We have conviction in the value of a global opportunity set, as opposed to a domestic, UK-centric investment approach. Historically, this has served clients well by reducing concentration risk, improving diversification, and accessing a fuller spectrum of global earnings and growth opportunities.

[1] Source: MSCI All Country World Index, as at February 2026